6th

June

Resurgence in five-year fixed rate deals

- Demand for five-year fixed rate remortgages jumps up 47% – representing half the market

- Five-year deals up 11 percentage points from March (as a proportion of the whole market)

- Expectations for an increase in the base rate this year fall to lowest level in seven months

- Average remortgage loan amount reaches £175,000 – a record high

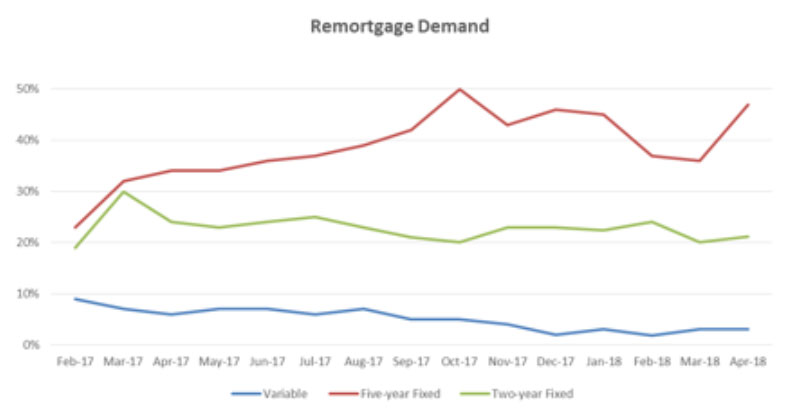

Demand for five-year fixed rate remortgages has bounced back to hit 47% of the total remortgage market in April – the highest proportion in six months, according to conveyancing service provider, LMS.

April’s resurgence is a significant increase from the previous month when five-year fixed rate deals made up just 36% of the remortgage market. Demand for five-year fixed deals is also 13 percentage points higher than April 2017 (34%).

This growth in popularity has been driven by an increase in borrowers switching from two-year deals to longer term deals as lenders provide more competitive offers to attract long term borrowers. The average rate for five-year fixed remortgages only increased by 0.01% month-on-month to reach 2.91% in April – well below the increase in the average two-year fixed rate.

The two-year fixed rate has risen 0.04% month-on-month to 2.43% in April – up from 2.20% in October. This is the highest two-year rate since September 2016, as lenders have amended rates to reflect the base rate rise.

The proportion of borrowers consulting an independent mortgage adviser or broker when remortgaging also hit a record high of 78% in April – increasing from 72% in March.

Nick Chadbourne, chief executive of LMS, said: “The popularity of five-year fixed rate deals rebounded in April, having dipped in the first three months of the year. Lenders are eager to attract longer term business which has created a competitive landscape for customers. This has ensured five-year average rates have remained relatively flat month-on-month. As more borrowers seek independent advice when remortgaging, the market is reacting quickly to the shifts in headline rates.

“Five-year fixed rate remortgages will always be popular when borrowers are seeking financial security. Many consumers are now opting for these deals to ensure they have certainty and stability through the potential economic and political upheaval of the next few years.”

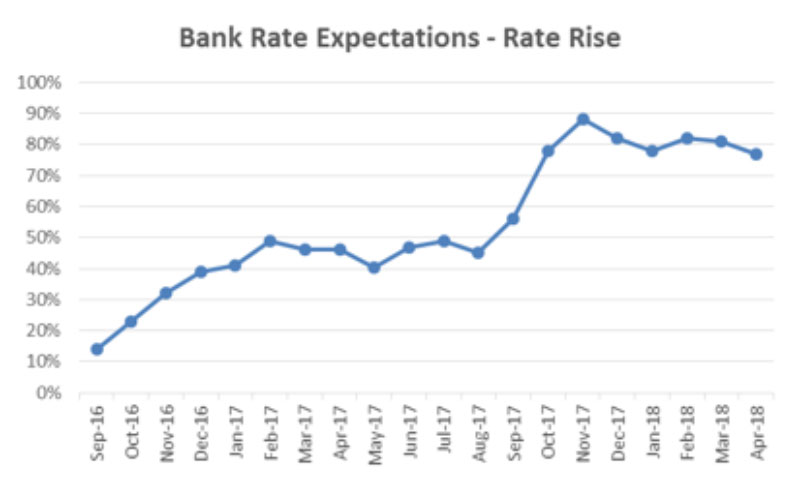

Expectation of a base rate rise in the next year falls to lowest level in seven months

The proportion of remortgagors who expect a base rate rise this year has declined to 77% – the lowest level in seven months. This is a 4 percentage point decline month-on-month.

However, expectations of an increase in the base rate are still significantly higher than they were in April last year when only 46% of borrowers believed there would be a rate rise in the year ahead.

Nick Chadbourne added: “After hints of a rate increase earlier in the year, sluggish economic growth discouraged the Bank of England from raising the base rate. Yet more than three quarters of borrowers still believe another base rate increase will happen at some point in the next twelve months. The surge in borrowers playing it safe by locking in longer term fixed-rates when remortgaging is understandable when the direction of the economy is so difficult to predict. Despite poor overall growth figures, unemployment and inflation are both falling – offering a very mixed, confusing economic landscape.”

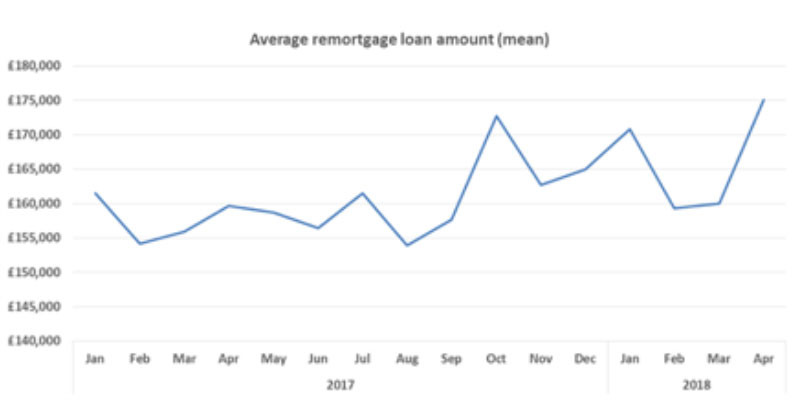

Average remortgage loan amount reaches record high

The average remortgage loan amount hit a record high in April of £175,000. This represent a 9% increase on March’s average of £160,000 and a 10% rise year-on-year. Property prices have only risen 1% year-on-year leading to higher loans to value ratios.

The term of a remortgage, as a three-month rolling average, increased to 58 months in April – up from 56 months in March. This is the longest term length since July 2016.

Nick Chadbourne said: “The average loan size jumped to a new peak in April as consumer take larger remortgages. With comparatively slow house price growth this month, LTV ratios have also increased. To balance the higher LTV ratios, the average term length has increased to the highest level in 21 months.”

– ENDS –

Please see LMS’ full Remortgage Report attached.

NOTES TO EDITORS

The methodology for calculating average LTV and loan amounts in regional areas changed in May 2016 and now uses the LSL House Price Index. Previously the ONS House Price Index was used which has since been combined with the Land Registry House Price Index.

FOR FURTHER INFORMATION

James Staunton: 020 7427 1404 or Henry Conner: 07709 577073 email LMS(Replace this parenthesis with the @ sign)instinctif.com

ABOUT LMS

LMS’s UK remortgage lending estimates are based on LMS’s up to date internal conveyancing data, which, every month, covers many thousands of remortgage completion transactions.

• LMS (Legal Marketing Services) is one of the UK’s largest providers of outsourced property services, including conveyancing, remortgage and IT services

• Each year LMS successfully manages over 200,000 transactions, helping to enable more than £30 billion in loans for intermediaries and lenders

• LMS develops and utilises cutting edge technology to ensure that its service meets lenders demands and remains at the forefront of the industry

• The LMS system is based on the company’s unique STARS (Servicer Tracking & Reporting System) technology which manages transactions electronically on-line to ensure speed, cost efficiency and quality of service

• To find out more about LMS, visit www.lms.com

Posted:06/06/18